Privatizing Scientific Medical Research Funding with a Multi-Value Tax Deduction

Background

Last updated: 3/24/2022 10:17 pm PST

I wrote "Privatizing Welfare By Funding It With a Double-Value Tax Deduction", which was published in ShareDebate International in June 26, 1994, which was one of the first electronic published magazines. For my new Substack magazine, “Towards a Humane & Sane Post Pandemic Society”, my lead article had as point #3: “Stop taxpayer funding of medical research, instead provide the incentives via a double-value or triple-value tax deduction approach for individual taxpayers to fund competing medical grant financial foundations. A double-value tax deduction, means a $1 given allows the individual to record on their taxes they donated $2.”

The below is pretty much that same original paper except instead of focusing on funding Welfare via this mechanism, it is on funding medical research. As much as possible, the wording is from that 1994 paper.

The Idea

My policy making philosophy is simple: in contrast to extremists that the ends justify the means, I contend that the means must be justified and that the means dictate whether the actualized ends are justifiable. Empirically, I believe that the choice of means almost always predetermines whether the desired ends will be obtained. The argument today about Medical Research varies between those liberals who are concerned about the need for it and those conservatives/libertarians who are concerned about the actual impacts how medical research is funded. They date have taken two positions that are self- defeating: either they argue for the abolition of the institutions behind medical research but the civic good-mindedness of the community rejects that or they have argued for restructuring the medical research infrastructure with a tax-based program which is still redistributionist and hence, non-conservative (as well as prone to political corruption). A third position can be advanced -- one that centers itself on the means -- how medical research is funded.

As a seated alternate to the 1994 Minnesota state GOP convention, I discussed the idea of funding welfare via a multi-value tax deduction with a few state legislators who asked for a detailed paper. I confirmed my hunch that under the existing welfare system, about 25 cents on the collected-tax dollar targeted for such finds its way into a welfare-recipient's hand. The balance goes to the tax collecting system and the welfare state bureaucracy. Yet private sector welfare agencies are able to pass along anywhere from 80-90 cents on the collected dollar to recipients.

The same insight and arguments apply to funding medical research!

Imagine the following medical research system -- keep in mind it is flexible enough to handle anticipated rare problems -- it's flexibility will be explained afterwards. Imagine the State (any of the 50 States) or Federal Government announces that medical research will henceforth not be tax-funded at all and instead will be funded by a multi-value state tax deduction and private sector Medical Research agencies. A double-value tax deduction (DVTD), as one example of a multi-value deduction approach, means that if an individual contributes one dollar to a private sector Medical Research agency, he or she is able to deduct two dollars as a charitable contribution on his or her income tax.

Immediately an astute reader has one concern: what about donations to non-Medical Research foundations or charities? To avoid having this double-value tax deduction drain away all charitable contributions to the existing single-value tax deductions (i.e., a dollar given is a dollar deducted), the tax law could require that the ratio of DVTD dollars must be a 1:2 ratio with single-value tax deducted dollars. That is, an individual if he or she wanted to donate $300 to private sector Medical Research agencies would have to also donate $600 to non-Medical Research private sector charitable/educational agencies in order for that $300 Medical Research donation to count as a double- value tax deduction. (In the absence of the 1:2 ratio, the contributor could still obtain a single value tax deduction, of course.)

By "private sector medical research agencies," I am referring to any lawfully recognized 501(c)3 charitable organization, whether religiously involved or not, whether locally based or nationally known. The proposed legislation will have to somehow provide a mechanism to distinguish those 501(c)3 charitable organizations that are engaged in funding qualified medical research operations versus those that aren't.

The State could require the following four items of information to be collected by the private sector medical research funding agencies: the social security number of the recipient, the dollar amount received, date, and tax ID number of the private-sector medical research funding agency. From the information collected, information can be summarized and reported in two forms: -- to the public, they will be able to determine which private sector medical research funding agencies are most efficient at getting recipients involved in public favored (or donor favored) medical research; -- to the private-sector medical research funding agencies, they will be informed if individual researchers (recipients) are also collecting money from other medical research agencies. Such can be deemed okay, it’s just that with multiple sources of funding, transparency is vitally important. The private sector charitable agencies should not have access to records in the original database that has real SSN data for people who are not receiving nor requesting to receive medical research funding from the individual agency.

The collecting of money from more than one private sector Medical Research agency would be totally legal, as long as the recipients are not lying under contract laws if any of the private-sector medical research agencies have their recipients sign forms stating they agree under private- sector contract law that they have filled out their form truthfully as a contractual condition for obtaining the private medical research assistance. You see, there is no need for state intervention in the agency forms and procedures used -- existing contract law can handle that. The only thing the State needs to concern itself with are the four items of information earlier listed -- the free market can handle the rest. You see, some medical research agencies may be more generous than others -- some may want to piggyback other agency's efforts. Let the donating private-sector determine by their voluntary contributions what agencies are worthy of their donations.

A modified duplicate of the State's database should be made public for private-sector scholarly analysis where the individual Social Security numbers (SSN) are randomly altered but in a consistent manner. For instance, a SSN of 123-456-7890 could become ABC-ZXY- EIMN but all occurrences of 123-456-7890 would become the same. Yet, 123-456-7891 might (under randomization) become HAT-BCE-MLOP. The idea is that there is no consistent algorithm to allow one to reverse the alteration from the alphabetized SSN to its’ original numeric SSN. [1]

In this medical research funding system, competition would be abundant. Existing charitable contributions would continue under whatever required ratio 1:2 tax law is made (discussed earlier). But the government only needs to spend a tiny fraction of it spends now to have medical research recipients receive the same amount of money! (It’s not really spending but “losing” some amount of taxes they’d otherwise collection without the multi-deduction. Tax funding would be required to maintain the four items of information collected, however, that too could be funded by filing fees applied to any soliciting medical research scientist.)

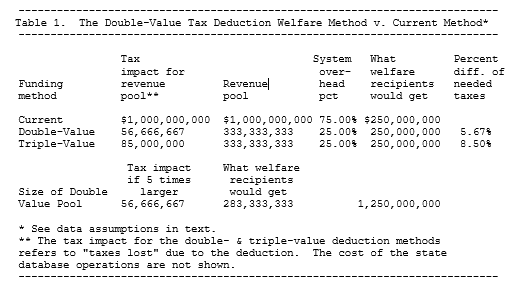

Look at Table 1 for an example of the funding advantages under discussion.

This assumes several things, first, that income taxes in the state average 8.5 cents on the dollar (my original paper aimed at state governments, not the federal government; adjust the amount if applied to the federal government. I still like the idea of having the primary audience be a state government. I can imagine Florida doing something like this far before the Federal Government.

A new tax deduction reduces state revenue from taxes collected by 8.5 percent of the amount deducted. DVTD would reduce state revenue from taxes collected by 17 percent of the amount deducted. One billion dollars from taxes collected for medical research now means $250 million to medical research recipients -- remember the other 75 percent goes to the cost of collecting taxes and the Medical Research bureaucracy. Assume that private sector Medical Research agencies, plus the cost of computerizing and reporting the gathered four pieces of information reduces the average efficiency of private sector medical research agencies to 75 cents on the dollar level (the existing range reported in the general press is between 80-95 percent efficiency). To get $250 million to medical research recipients via the DVTD method requires only $56.7 million of "lost taxes" due to the tax deduction. 17.6 times less revenue is required!

A liberal state, such as Minnesota, could adopt this method and allow up to five times as much money to be given to recipients than the existing system yet still reduce the tax burden by over 71 percent!

The table on the next page shows the mathematics involved. In the table is a reference to "triple-value funding" -- I'll explain that later.

The Moral Benefits

The worst thing about Medical Research today, as it is has been funded since the days of its’ earliest funding, going back to the start of the 20th century, is that the money collected is through the power of the gun -- the power of the state that backs the tax law rests on force that will be used if the taxes are refused. The message sent by the current funding method is that the recipients consider it a guaranteed entitlement -- a governmental right.

Under the DVTD Method, no such message will be sent to medical research recipients. The giving is entirely voluntary. Not a single individual is forced to make the donation to obtain the tax deduction. It isn't taxes collected but tax revenue lost by the existence of the deduction. Recipients will know that the money they receive is through the generosity and support of their fellow citizens. People do not make money or save money through tax deductions. If I donate a dollar under the DVTD method, I reduce my state taxes by 17 cents but I reduce my retained revenue by one dollar. Yet Americans are very generous people. They will give to private sector medical research agencies.

One legislator in the early 90s asked me what if up-state people in the countryside do not give enough to private sector Medical Research agencies? Well, some of the metro (down-state) donations could be to state-wide private sector agencies. Secondly, if the DVTD method is not pumping enough money into private sector Medical Research agencies, the state could make it a triple-value tax deduction. That is, a dollar donated is a three dollar tax deduction. Table 1 presented above shows how even a triple-value tax deduction reduces the impact on tax revenue 11.7 times less!

What is the difference in this moral message? Under the DVTD method, individuals will feel grateful to the goodness of private-sector individuals and not to big government.

This is obviously a conservative philosophy approach to funding Medical Research. I hope readers will broaden their appreciation for this approach and read the historically insightful book of Marvin Olasky, The Tragedy of American Compassion (Washington, D.C.: Regnery Gateway), 1994.

Meeting Various Obstacles

Mr. John H. Fund in the June 14th, 1994, Wall Street Journal editorial page, in "Medical Research: Putting People First," advocates a similar approach but using a tax credit versus a modified tax deduction. The problem with a tax credit is that it impacts tax revenue 5.88 times as much as the DVTD method and the message sent to recipients is no longer that of love--for giving is no longer a voluntary financial sacrifice of the giver- -the sacrifice is no longer there. Furthermore, Mr. Fund's approach lacks the information feedback that exists in the DVTD method and without that, recipients could abuse the system through approaching multiple, competing private-sector Medical Research agencies and the underclass could conceivably grow.

Last, to pass this proposal, there will have to be more political groups behind it than for maintaining the existing system. If we advocate the generous approach of reducing the impact on state tax revenue by threefold but increasing the pass-through revenue to recipients by fivefold, it should be easy to get medical research recipients to vote for the change -- it's been said that change is always resisted unless the improvement is seen as overwhelmingly to one's benefit. With the ratio of DVTD to normal charitable tax deductions 1:2, or whatever it must be to gain the support of existing charitable organizations, it will be greatly advantageous to these private sector organizations for they will see tremendous growth. Conservatives, including medical research-conservative minded Democrats, should naturally favor the DVTD method over the current method or any tax-funded workfare approach. That leaves the Medical Research bureaucrats and diehard statists as the main opponents of DVTD. Given a good campaign, DVTD should be easy to pass into law, especially if it tried and succeeds at a county level first.

The above paragraph was written in 1992. In the era of the heavily corrupted, deep Medical State that led to the post Covid-19 pandemic crisis, I can imagine medical researchers desperate for an alternate funding approach if the widespread public revolt against the Medical State is to defund and abolish the FDA, CDC and NIH. This is not too farfetched if the public learns of the reason for the statistically, prolonged increase in all-cause mortality, being written about by many Substack writers. See my “reads” on my Substack Profile page.

DVTD can be easily tuned to fit unfavorable conditions by adjusting either the tax deduction -- go for a triple-value or quadruple-value tax deduction for instance, or by adjusting the DVTD to normal tax deduction donation ratio -- perhaps 1:2 or 1:3 or 1:4. Because of this flexibility, target spending can be approximately met even though this is not a central-planning/funding setup.

The main point is that with the double-value tax deduction method, the means are justifiable and are most likely the best means to obtain ends that we can justify proudly. Free market competition in charity will rule and once again, as the generous in America did in the 19th century, we can be seen as caring neighbors in the community to those who will be helped in an environment of freedom to choose which method (source of help) do they want to turn to for help in finding research answers for health problems. Just as the well-off people have freedom of choice, let's enable all Americans to have freedom of choice to determine how and why we are faced with so many health problems!

For instance, the CDC has a page on autism. In 2009, it stated “an average of 1 in 150 children in the United States have an ASD [Autism Spectrum Disorders].” In 2022, this same CDC page asserts: “About 1 in 44 children has been identified with autism spectrum disorder (ASD) according to estimates from CDC’s Autism and Developmental Disabilities Monitoring (ADDM) Network.” Yet Robert F. Kennedy in his must-read book, “The Real Anthony Fauci” writes on page 526: “In 2014, another CDC whistleblower, the agency’s senior vaccine safety scientist, Dr. William Thompson, disclosed that top CDC officials had forced him and four other senior researchers to lie to the public and destroy data that showed disproportionate vaccine injuries—including a 340 percent elevated risk for autism—in Black male infants who received the Measles, Mumps, Rubella (MMR) vaccine on schedule.”[2]

Does anyone realistically expect our current established medical research infrastructure to fund research that explains the causes and potential (well researched) solutions for Autism? Does anyone have faith that the FDA or CDC will ever give off-label, established safe, patent-expired drugs a chance at helping in any disease? We well know that the Medical Deep State favors under-patent protected drugs that enrich Big Pharma. Look at how Ivermectin, Zinc, Vitamin D, and Hydroxychloroquine was considered for Covid-19, despite the many hundreds of well researched reports done internationally. See https://c19early.com/ which currently has the title “COVID-19 early treatment: real-time analysis of 1,547 studies”.

The same goes for other areas of medical research. The areas I want to see privately funded to forward real advances in healthcare are the following:

· The use of one’s own Adult Stem Cells or one’s own Platelet Rich Plasma in Regeneration Injection Therapy (aided by ultrasound guidance) to deal with orthopedic problems now heavily skewed towards remedies that enrich Big Pharma and Big Hospitals. See https://regenexx.com/resources/ebooks-and-reports/ and https://regenexx.com/resources/research/. A lay introduction is given here.

· The use of the Metabolic Theory of Cancer to stop the reproduction of Cancer Cells using a multitude of safe, inexpensive, and cheap remedies (none of them patentable) versus the toxic remedies used to mostly unsuccessfully treat Cancer. Read Tripping Over the Truth: The Return of the Metabolic Theory of Cancer Illuminates a New and Hopeful Path to a Cure particularly the appendices where links to successful approaches to Cancer are detailed. Also see Cancer as a Metabolic Disease: On the Origin, Management, and Prevention of Cancer 1st Edition, by Thomas Seyfried, PhD.

· Facilitating the regenerative benefits of intermittent and moderately prolonged fasting through research that shows what a person can drink or eat but still maintain a state of Autophagy. Also read the book, The Complete Guide to Fasting: Heal Your Body Through Intermittent, Alternate-Day, and Extended Fasting by Jimmy Moore and Jason Fung, M.D. Also see books on Fasting-Mimicking Diets, such as “The Longevity Diet” by Valter Longo. And “KetoFast: Rejuvenate Your Health with a Step-by-Step Guide to Timing Your Ketogenic Meals” by Dr. Joseph Mercola.

· Safe Anti-Aging through low dose (taken weekly or bi-weekly) of Rapamycin. See https://rapamycintherapy.com/

Questions and Answers

I submitted the initial draft of this proposal, which was aimed at funding Welfare in the early 1990s, to newsgroups on the Internet and on Compuserve. I received very enthusiastic support for the proposal--no opposition--but I did receive several questions for which the answers are hard to retroactively fit into the main text. These questions and answers follow. Please note that the questions and attitudes in these questions are not mine! Some of the attitudes in these questions are harsher than my own!

Question 1: "On the whole, I like the idea. However, I am not sure of the justification of the 1:2 requirement. Allowing for my incomplete knowledge of relevant law, aren't all charities set up for public service in one form or another? Should medical research charities be singled out over, say, the Red Cross, or the local community theater? Do Goodwill and the Salvation Army count? How about the United Way? Where is the line drawn on Medical Research vs. non-Medical Research charities? I would prefer to see the double tax deduction for all charities."

Answer 1: In the public's eye there are two types of public services needed -- those that are so vitally a matter of life and death that the public has decided not to leave them to voluntary contributions such as medical research versus those considered of a lesser urgency but still desired for which the public allows them to have a tax-deduction status but funding is otherwise left up to voluntary contributions. This proposal maintains that distinction and separates the two "camps" via the single versus the multiple-value tax deduction (i.e., in case the double-value tax deduction does not raise enough money, the concept allows a triple-value, etc., tax deduction to be created). As said earlier, the enabling legislation will have to have a mechanism to distinguish those charities engaged in medical research versus non-medical research operations.

Question 2: "Will there be a tax reduction for everyone since the state will no longer be paying for medical research?"

Answer 2: There would be a reduction in state government spending equal to the amount of the current medical research setup. Taxes collected will be reduced the same less the small fraction of "taxes lost" due to the tax deduction (see the data table shown above).

Question 3: "How does the federal portion of Medical Research fit into your plan?"

Answer 3: The state would apply for a waiver from federal government and the U.S. Congressmen/Senator from the State would be wise to ask for whatever money it's entitled to to go to other projects however I'd prefer a tax rebate to taxpayers.

Question 4: "How is the benefit amount determined?"

Answer 4: Totally left up to individual agencies and the marketplace. Significant abuse would not be able to happen because of the database/reporting features. Any abuse would be made public and the marketplace would stop donating. Normal 501(c)3 charitable laws would be in force to prevent criminal abuse by the private sector agencies.

Question 5: "Will the recipient ever have to go to more places under your plan than they do today?"

Answer 5: That may or may not be the case--but if they do, the agencies handing out benefits, work or money to them will be told via the database reporting mechanism.

Question 6: "How does the recipient determine which agencies they go to?"

Answer 6: The same way people make decisions about the marketplace today--they learn from advertisements, word of mouth, libraries, or consumer guide agencies.

Question 7: "Please explain how the different agencies can give different benefits. If I was an agency I would give all the money to one recipient-- myself!"

Answer 7: You'd be in violation of 501(c)3 charitable contribution laws and quickly be in deep trouble. Nobody would want to donate to any agency that isn't a 501(c)3 charitable agency. Each 501(c)3 agency has information they publish that they use to attract donations. Within the constraints of 501(c)3 laws and marketplace feedback with the database reporting mechanism, different agencies can do very different things. That's the whole idea--to introduce consumer/payor-marketplace sensitivity and competition to medical research.

Footnotes

The author has a Master's degree in Sociology (1977) and works in the private sector as a healthcare database analyst (for over 33 years!). He regularly posts, under his full name, on Gab, MeWe, and rarely anymore, Facebook (whose censorship and shadow banning is atrocious). His email address is roleigh@pobox.com.

1. Researchers do not need SSN data but statisticians wants raw data so that they have control over aggregation and disaggregation analysis; hence the need to scramble SSNs because the SSN data is too confidential to be made public to them. However, the private sector medical research funding agencies need to be informed if their benefactors are getting contributions from more than one agency (which again, if individual rules allow it, would be okay; but it would be up to individual agency rules--all enforced by contract law if they so wish); hence the need for a database with the SSN data kept intact. Thus two databases are needed.

2. Kennedy Jr., Robert F . The Real Anthony Fauci: Bill Gates, Big Pharma, and the Global War on Democracy and Public Health (Children’s Health Defense) (p. 526). Skyhorse. Kindle Edition.

Such a fantastic idea to shift the motivation for research toward actual human health, understanding and advancement, instead of simply creating a profit center to keep the roundabout turning.